News / 14 June 2026

Weekly Review: Blast Off

The defining story of the week was SpaceX making its long-awaited stock market debut in what became the largest IPO in history. Trading under the ticker SPCX on the Nasdaq, the stock surged 19% on its debut, closing at around $161 and briefly trading as high as $176.52 before extended-hours buying pushed the implied market cap above $2.2 trillion. The $75 billion raised in the offering is the largest in history by a considerable margin. Elon Musk, who flagged on a pre-IPO JPMorgan livestream that SpaceX has been cash-flow positive since roughly 2015, framed the listing as capital-raising for a “significant growth phase”, one that includes putting over 100,000 satellites in orbit and building AI data centres in space. It is worth noting that Starlink remains the only profitable segment of the business today. The IPO also made Musk the world’s first trillionaire, based on his combined stakes in SpaceX and Tesla.

Beyond the blockbuster debut, broader equity markets managed to close the week in positive territory despite a turbulent ride. Small-caps led the charge, while the S&P 500, Dow and Nasdaq each added over 0.65%. The week’s dominant macro theme remained the U.S.-Iran conflict. Markets swung between risk-off and risk-on as missile exchanges, threatened U.S. strikes, and then President Trump’s last-minute cancellation of those strikes all played out in rapid succession. By Friday, cautious optimism around a potential peace deal was the prevailing mood.

The U.S. inflation picture this week was a study in contradictions. Headline CPI came in at 4.2% year-on-year in May, the highest since April 2023, driven largely by the energy shock from the Strait of Hormuz closure. On a month-on-month basis, however, CPI rose just 0.2%, below expectations and the second consecutive month of decelerating price growth. Core CPI similarly moderated, rising 0.2% versus 0.4% the prior month. Producer prices told a different story, with PPI jumping 1.1% month on month, well above the 0.7% consensus, as energy goods rose 10.7%. Year on year, PPI hit 6.5%, the highest since November 2022. The components that feed into core PCE, the Fed’s preferred gauge, are now pointing to a 0.4% print, which, if realised, keeps a rate hike firmly on the table before year-end. Consumer sentiment edged up to 48.9 in June, a 4.1-point improvement from May, helped by early-month easing in petrol prices, although the mood remains cautious with year-ahead inflation expectations sitting at 4.6%.

EUROPE & UK

In Europe, the European Central Bank delivered its first rate hike since September 2023, raising three key rates and flagging an “uncertain” outlook with upside inflation risks and downside growth risks. Updated forecasts now put eurozone inflation at 3.0% in 2026, moderating to 2.0% by 2028, while GDP growth was revised down to 0.8% for 2026. European equity markets were mixed on the week, though sentiment improved sharply on Friday as peace-deal optimism took hold. In the UK, April GDP contracted 0.1% month on month, a reversal from March’s 0.3% growth, with services the main drag. The data reinforced expectations that the Bank of England would hold rates at its 18 June meeting, while the FTSE 100 added 1.0% for the week.

ASIA

In Japan, the Nikkei fell 0.85% over a volatile week, recovering sharply on Friday alongside the broader geopolitical de-escalation. The Bank of Japan is widely expected to raise rates by 25bp to 1.0% at its 15-16 June meeting, its first hike since December 2025, while the yen remained pinned around JPY 160 to the dollar. In China, the picture was mixed: the Shanghai Composite was flat on the week (+0.09%), while Hong Kong’s Hang Seng fell 0.98% amid weaker offshore sentiment.

GLOBAL EQUITIES

Global equity markets pushed higher despite the volatility, with small-caps leading and the major U.S. benchmarks each gaining over 0.65%. In commodities, gold held around $4,200/oz but was on track for a second consecutive weekly decline as rate-hike expectations weighed on the metal. Brent crude fell 3.4% to $87.3/barrel on Strait of Hormuz reopening hopes, leaving oil down roughly 6% on the week, though prices remain over 20% higher since the initial U.S.-Israel strikes on Iran in late February. Looking ahead, the market’s focus turns to the Federal Reserve’s first policy meeting under new Chair Kevin Warsh. A hold is fully priced in, but the forward guidance matters enormously, specifically whether Warsh signals openness to hiking later this year.

Market Moves of the Week:

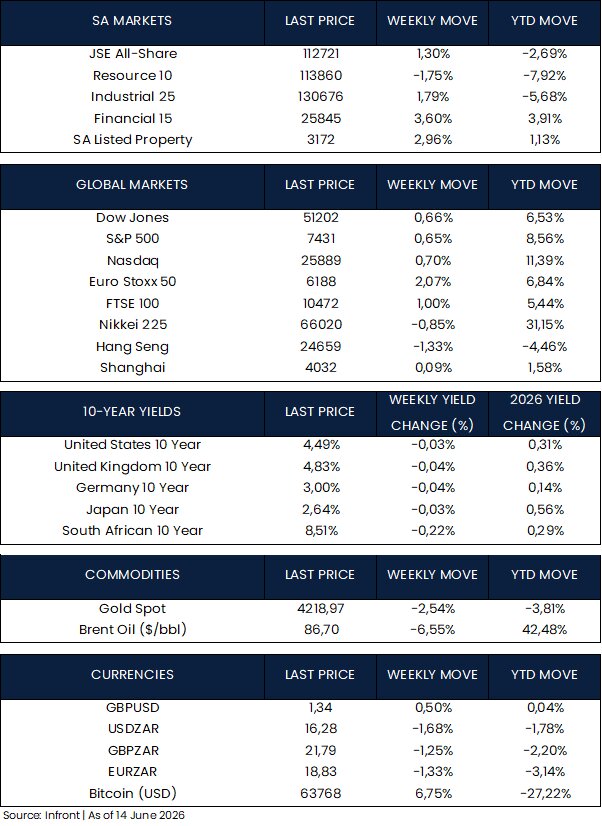

The domestic highlight of the week was the Q1 2026 GDP print, which came in ahead of expectations. South Africa’s economy expanded 0.5% quarter on quarter, up from 0.4% in Q4 2025 and the sixth consecutive quarter of growth, beating the Bloomberg consensus of 0.3%. On an annual basis, growth accelerated to 1.9%, also ahead of the 1.8% forecast. Finance, real estate, agriculture, trade and transport were the primary drivers, with agriculture posting its sixth straight quarter of expansion at 3.9%. The numbers are encouraging on the surface, but the detail warrants some caution, as fixed investment declined despite the broader expansion and domestic demand remains soft.

On the ratings front, Fitch upgraded South Africa to BB on 5 June, moving it in line with Moody’s and S&P, both of which also carry positive outlooks. National Treasury welcomed the move as an endorsement of fiscal policy and a signal that investment-grade status is within reach if reform momentum holds. South African assets have also benefited from the country’s removal from the FATF grey list and the Reserve Bank’s adoption of a 3% inflation target last year, a policy shift that delivered a meaningful decline in government bond yields. The benchmark 10-year yield is now roughly 150 basis points lower than a year ago, and the rand, despite modest weakness since the Middle East conflict escalated in late February, remains about 9% stronger against the dollar year on year, trading at R16.28 this week versus R16.55 last week.

The JSE All Share closed the week up 1.3%, with financials, industrials and listed property all firmly in the green. Resources underperformed on the week, weighed down by the commodity price volatility tied to Middle East uncertainty.

Chart of the Week:

SpaceX stole the headlines this week, making its long-awaited stock market debut in what became the largest IPO in history. Trading under the ticker SPCX, shares opened at $150 and surged as high as $176.52 before closing at around $161, a 19% gain on day one, valuing the company at $2.1 trillion. Extended-hours buying added another $100 billion to that figure. The $75 billion raised in the offering eclipses every IPO that came before it, and with over 500 million shares changing hands, the debut drew comparisons to Facebook’s first day in 2012, which saw roughly 580 million shares traded. Source: NASDAQ

Credits: Strategiq Capital