News / 11 June 2026

MONTHLY MARKET OVERVIEW & COMMENTARY | MAY 2026

May delivered another positive month for global equities, although market leadership remained narrow and concentrated in companies linked to artificial intelligence. Investors focused on resilient earnings and structural growth themes, while improving US-Iran negotiations toward month-end helped ease pressure on energy markets.

South African markets lagged global peers, with the FTSE/JSE All-Share down 0.48% in May and 1.04% lower year-to-date. Sector performance was mixed: financials (+0.82%) and listed property (+0.62%) gained, while resources (-1.67%) and industrials (-0.93%) declined. The local market’s limited exposure to AI chipmakers, which drove global and emerging market returns, contributed to its underperformance.

Globally, equities advanced strongly. The S&P 500 (+5.15%), Dow Jones (+2.78%) and Nasdaq (+8.36%) all gained, supported by earnings and technology momentum. Japan (+11.45%) was the standout performer, Europe also advanced, and China weakened as concerns around domestic demand persisted.

Bond markets remained volatile as investors weighed oil-driven inflation risks against possible geopolitical de-escalation. The US 10-year yield ended May at 4.44%, while the South African 10-year yield declined to 8.39%, supporting local fixed income. Local bonds and the rand were also helped by attractive yields and a more constructive fiscal outlook.

TRENDS THIS MONTH:

-

Global equities advanced, led by AI-related technology and semiconductor shares, although market leadership remained narrow.

-

US earnings remained resilient, but inflation pressures and the change in Federal Reserve leadership kept interest-rate expectations in focus.

-

Oil prices eased as US-Iran negotiations improved, although inflation risks remained elevated.

-

South African equities lagged global peers, while the rand and local bonds were supported by the SARB’s 25bps rate hike, attractive yields and improved appetite for local assets.

MIDDLE EAST CONFLICT: OIL EASES, INFLATION RISKS REMAIN

The Middle East remained one of the key macro drivers in May. The continued restrictions through the Strait of Hormuz kept energy markets under pressure for much of the month, although negotiations between the US and Iran appeared to improve toward month-end. This raised hopes that the conflict could move closer to resolution and that normal activity through the Strait could gradually resume.

Oil prices eased sharply from the elevated levels seen earlier in the month. However, the inflationary impact of the earlier energy shock remained important, and central banks continued to face a difficult balance between managing higher energy-driven inflation and avoiding unnecessary pressure on growth. Markets are now balancing two competing scenarios: de-escalation, where lower energy prices could support both equities and bonds, and slower normalisation, where oil prices could remain above pre-crisis levels, keeping inflation expectations elevated.

UNITED STATES: AI AND EARNINGS LEAD MARKETS HIGHER

Equity Performance:

-

Dow Jones: +2.78%

-

S&P 500: +5.15%

-

Nasdaq: +8.36%

US equities delivered strong gains in May, supported by a resilient earnings season and renewed momentum in technology shares. The rally was particularly concentrated in AI-related areas, where demand for computing power, semiconductors and infrastructure remained a major driver of investor interest.

The macro backdrop was more mixed. Inflation remained elevated, with higher energy prices feeding into headline CPI, while producer prices also pointed to ongoing cost pressures. At the same time, labour market and retail sales data remained firm enough to reduce fears of a sharper slowdown. Monetary policy also remained in focus after Kevin Warsh was sworn in as Federal Reserve Chair, with higher oil prices and inflation concerns pushing markets to price in a higher path for interest rates.

Outlook: The US remains a key driver of global markets, but performance is increasingly concentrated in a narrow group of growth and AI-related companies. This supports returns in the near term but also increases concentration risk.

EUROPE: GAINS DESPITE SOFTER MACRO DATA

Equity Performance:

-

Euro Stoxx 50: +2.87%

-

FTSE 100: +0.29%

European equities advanced in May, supported by stronger global sentiment and positive earnings, although returns lagged the strongest global markets. The region remained sensitive to energy prices and softer growth momentum, with eurozone growth forecasts revised lower and inflation expectations revised higher. In the UK, weaker labour data and lower-than-expected inflation helped gilts perform better, while political uncertainty remained a risk.

Outlook: Europe continues to offer diversification, but performance remains closely linked to energy prices, growth expectations and central bank policy.

JAPAN: STRONG MOMENTUM CONTINUES

Equity Performance:

- Nikkei 225: +11.45%

Japan was one of the strongest-performing major markets in May. Equity gains were supported by technology and semiconductor shares, as investors continued to favour markets with exposure to the AI theme. Japan’s first-quarter GDP also came in ahead of expectations, while softer inflation data reduced near-term pressure on the Bank of Japan to tighten policy. This combination of stronger growth data and reduced policy pressure supported investor sentiment.

Outlook: Japan continues to benefit from global technology and AI demand, but remains sensitive to currency movements, energy prices and bond yield volatility.

CHINA: GROWTH CONCERNS PERSIST

Equity Performance:

- Shanghai Composite: -1.06%

Chinese equities delivered a weaker month, with investors remaining cautious about the domestic recovery. Services activity showed some resilience earlier in the month, but later data pointed to slower industrial production growth, weak retail sales and ongoing uncertainty around external demand. Policy support remains important, but investors continue to question whether current measures will be enough to stabilise domestic momentum.

Outlook: China remains a selective opportunity, with performance likely to depend on the strength of policy support and signs of improvement in domestic demand.

SOUTH AFRICA: LOCAL MARKET LAGS GLOBAL PEERS

Equity Performance:

-

JSE All-Share: -0.48%

-

Resource 10: -1.67%

-

Industrial 25: -0.93%

-

Financial 15: +0.82%

-

SA Listed Property TR: +0.62%

South African equities ended May slightly lower, underperforming global and emerging market peers. Resources were weaker as gold’s recent tailwind faded, while industrials also declined. Financials and listed property performed better, supported by improved appetite for local assets and lower local bond yields.

The rand was a stronger point for local markets, supported by attractive yields, improved appetite for local assets and the South African Reserve Bank’s decision to raise rates by 25 basis points. The hike followed April inflation rising to 4.0% year-on-year and reflected the Bank’s intention to stay ahead of energy-driven price pressures.

Outlook: South African assets continue to offer attractive yields, but equity performance remains heavily influenced by global drivers, commodity markets and currency movements.

CURRENCIES: RAND STRENGTHENS

Key Moves:

-

GBP/USD: -1.16% (1.34)

-

USD/ZAR: -2.72% (16.21)

-

GBP/ZAR: -3.85% (21.81)

-

EUR/ZAR: -3.19% (18.93)

Currency markets were supportive for South Africa during May. The rand strengthened against the dollar, pound and euro, helped by improved local sentiment, attractive yields and the SARB’s rate hike.

Takeaway: Rand strength provided some support to local markets, although the currency remains sensitive to global risk appetite and commodity dynamics.

FIXED INCOME: MIXED YIELDS AS INFLATION RISKS PERSIST

10-Year Yields (End-May | MoM change):

-

United States: 4.44% | +0.07%

-

United Kingdom: 4.81% | -0.23%

-

Germany: 2.93% | -0.10%

-

Japan: 2.66% | +0.13%

-

South Africa: 8.39% | -0.41%

Bond markets were volatile during May as inflation expectations shifted with oil prices and US-Iran negotiations. South African bonds performed well, with the local 10-year yield moving lower despite global inflation concerns.

Takeaway: Fixed income remains sensitive to energy prices and central bank expectations, but easing inflation pressure could provide support if oil prices continue to normalise.

FINAL THOUGHTS: STRONG MARKETS, NARROW LEADERSHIP

May reinforced the market’s willingness to look through geopolitical uncertainty when earnings are strong and structural growth themes remain powerful. Global equities delivered solid gains, but leadership was narrow and heavily concentrated in AI-related areas.

What this means for portfolios: maintain diversification, as market leadership remains concentrated; balance growth exposure with defensive assets, given ongoing inflation and geopolitical risks; and use global diversification to reduce reliance on any single region or sector.

While May was positive for global equities, the underlying environment remains complex. A diversified and disciplined approach remains important as markets continue to navigate narrow leadership, uncertain energy dynamics and cautious central banks.

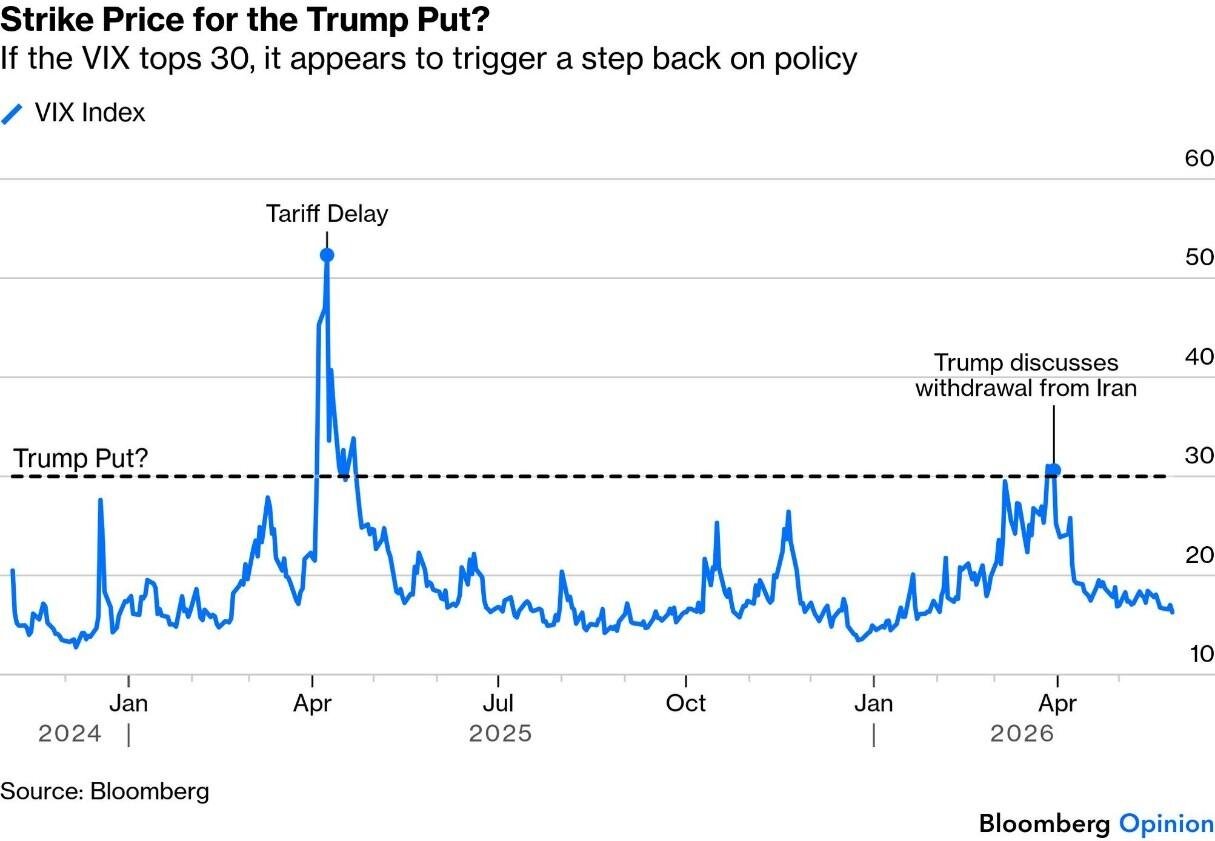

CHART OF THE MONTH:

The VIX has fallen sharply from above 30 to below 16, reflecting a clear easing in market stress as lower oil prices and hopes of progress in the Middle East supported risk appetite. However, the chart highlights that volatility remains an important pressure point for markets, with any renewed geopolitical escalation likely to quickly test investor confidence again. Source: Bloomberg

Credits: Strategiq Capital, Bloomberg